At the risk of sounding like Nick Cannon on the television show America’s Got Talent when they’re announcing performers advancing to the next round of competition, employers are beginning to see the results of appeals that they’ve filed when employees receive subsidies in the marketplace. Employers are finding some of these appeal decisions perplexing, especially when an appeal is denied. And, some employers fear that penalties will follow as a result of the lost appeal.

First, and of most importance, the marketplace appeal does not determine if an employer has to pay an employer shared responsibility penalty to the IRS. This point is made clear on both the appeals form and on the webpage that addresses employer appeals.

Second, an appeal that is denied may be due to the particular facts and circumstances of the employee and his/her family. In particular, even though an employer may have offered coverage that meets the minimum value and affordability safe harbors, the measure of affordability at the marketplace is based on household income. Household income may be quite different from an employee’s W-2 income. The marketplace’s decision regarding an employer’s appeal will not reveal personal and income information of the employee subject to the appeal.

The appeal decision letter explains that the marketplace will not consider whether an employee is a full-time employee or whether the employer employs 50 or more full-time employees and is subject to the employer shared responsibility payments. The reasoning cited in the letter is that “neither of these issues affect the employee’s eligibility for advance payments of the premium tax credit and cost-sharing reductions (if applicable).

Another employer found that the information which the employer sent to support their appeal did not go far enough. The employer submitted proof that the employer had offered coverage to the employee that met minimum value and was affordable. The hearing officer wanted proof of this offer in the form of the employee’s response to the offer. Employers that have been reluctant to require that employees sign waivers when they decline coverage may decide to require signed waivers or take other steps that can buttress the fact that an offer was made and rejected.

A review of several decision letters finds that decisions often cite “insufficient information” as the basis for the decision to reject the appeal. Employers may want to develop a checklist of materials that they will provide to ensure that appeals are not lost for want of more information.

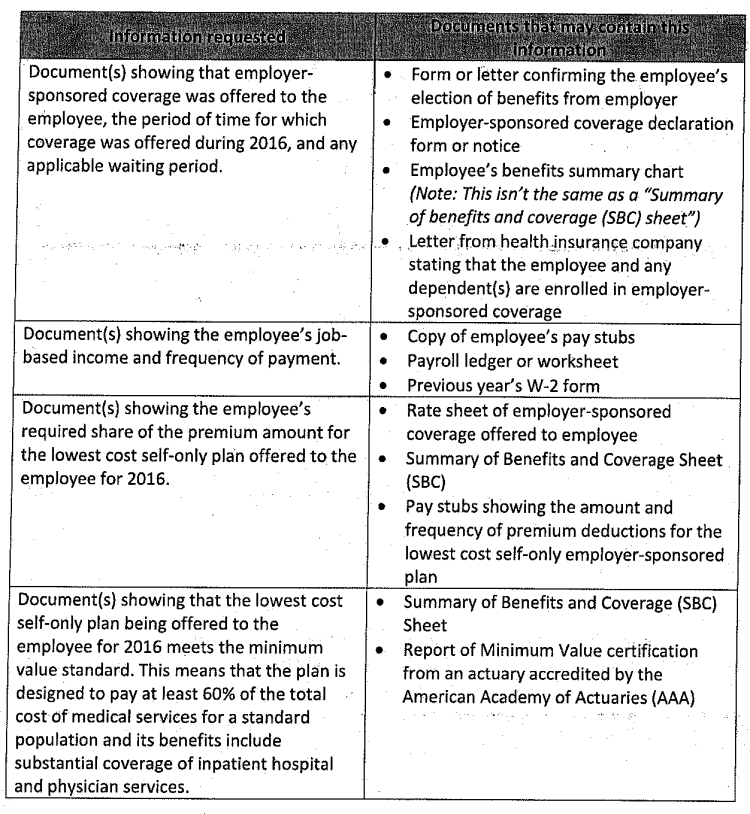

Still other employers have received a letter while an appeal is under review that asks for more information to support the appeal. The types of information requested and documents that may contain the requisite information are shown below in a table copied from a letter asking for more information.

While marketplace appeal decisions are not triggers for IRS penalties, a successful marketplace appeal may be helpful if the IRS does attempt to penalize an employer. The successful appeal would be another piece of information for an employer to include in the IRS appeal’s process. And, whether an appeal is successful at the marketplace level, or not, an employer will have already collected information that would be required to appeal an IRS penalty determination should one be received.