IRS Notice 2015-60 brought some bad news to employers with health plans. The notice announced the PCORI fee will increase for health plan years that end on or after October 1, 2015 and before October 1, 2016.

The fee is rising from $2.08 per covered life to $2.17 per covered life, an increase of 4.3 percent. PCORI fee payments are due July 31 of each year. The fee is slated to expire for plan years ending by October 1, 2019.

The amount of the PCORI fee is “equal to the average number of lives covered during the policy year” multiplied by the fee amount. It’s important to note that the PCORI fee is based on “belly buttons” not the employee count. An employer and dependent child count as two (2) covered lives.

Employers are facing the impending deadlines for the ACA’s employer reporting requirements. As of today there are only 116 calendar days left until employers have to file statements to full-time employees! Employers who are required to report are generally those who meet the definition of “applicable large employer” or ALE.

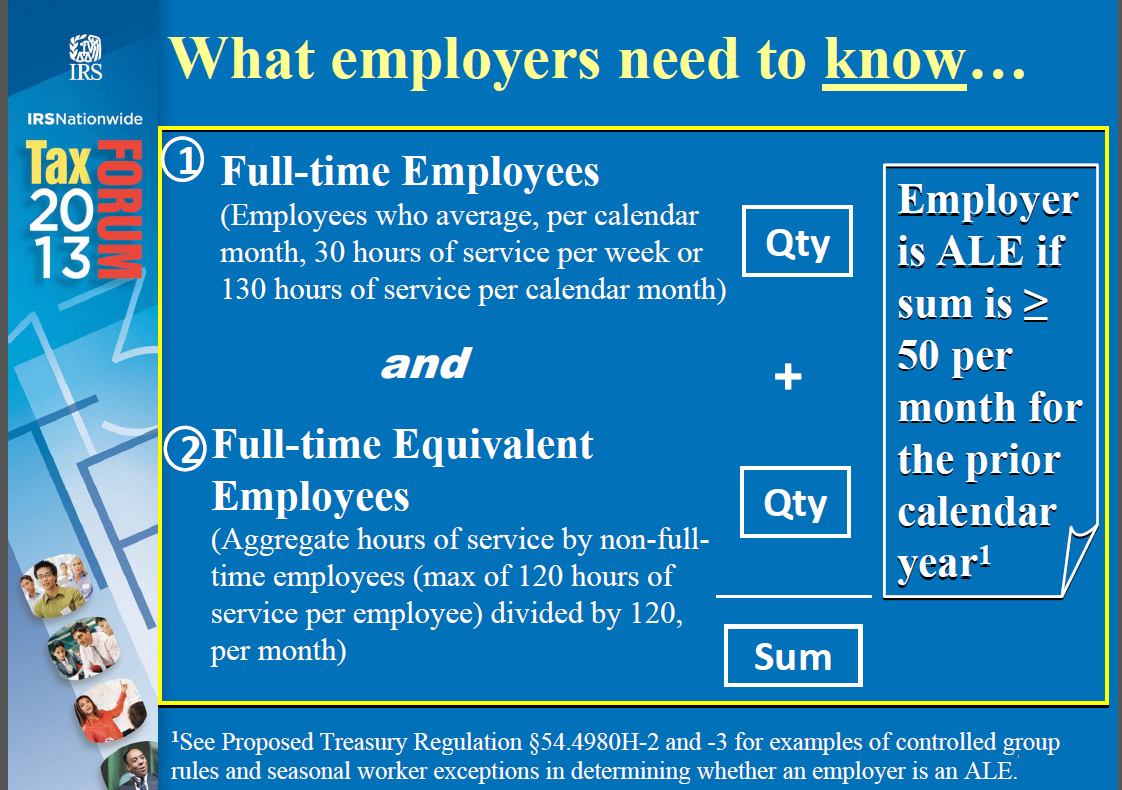

ALEs are employers with 50 or more full-time and full-time equivalent employees. For a refresher on calculating ALE status see our August 13, 2015 blog post.

Form 1095-B and form 1095-C statements must be furnished to covered individuals or full-time employees, as applicable, on or before January 31. In 2016, the deadline is February 1, 2016 since January 31st is on a Sunday.

An ALE must file Form 1094-C and Form 1095-C with the IRS on or before February 28 (March 31 if filed electronically). In 2016, the deadline is February 29 since the 28th is a Sunday.

Employers who need extra time to file their reports, may find some relief. Employers needing more time to file can apply for an automatic 30 day extension. They must file Form 8809 by the filing deadline. This is the same form that an employer would use to request an extension of the deadline for filing the Form W-2. http://www.irs.gov/pub/irs-pdf/f8809.pdf

It’s important to note, however, that the automatic extension of time to file will only extend the due date for filing the information returns with the IRS. It does not extend the due date for furnishing statements to recipients.

Form 1094-C is the transmittal form that is sent to the IRS along with a firm’s Form 1095-Cs. As noted in an earlier blog, this form is far more complicated and confusing than a mere “transmittal form” would suggest.

As a reminder, the option on line 22 are:

Qualifying Offer Method

Qualifying Offer Method Transition Relief

Section 4980H Transition Relief

98% Offer Method.

You can’t complete line 22 of Form 1094-C unless you decode the options listed as “certifications of eligibility.” We have previously decoded what a “qualifying offer method” entails. Here’s the scoop on Option D, the 98% Offer Method.

Option D, the 98% Offer Method, is also hard to qualify for. It requires that:

Employer that is an ALE (applicable large employer) offered for all months of the calendar year, affordable coverage that provided minimum value to at least 98% of employees receiving Form 1095-C

MEC to dependents.

What’s the payoff for offering this generous coverage? An employer that meets these requirements doesn’t have to complete Part III, column (b) of Form 1094-C (the full-time employee count).

What’s the catch? Perhaps the better question is “that’s a payoff”? This may be a consideration if an employer has difficulty determining which employees are full-time.

Form 1094-C is the transmittal form that is sent to the IRS along with a firm’s Form 1095-Cs. It has been compared to a FAX cover sheet. A FAX cover sheet for those too young to remember was used to identify the person who was to receive the information. The cover sheet often gave a brief overview of any pages that were included as a part of the FAX transmission as well as the number of pages that were being sent.

Simply put, the Form 1094-C is far more complicated than a FAX cover sheet ever was!

In fact, one line on the form would benefit from another even more historically remote object – a decoder ring! Line 22 certifies for employers, where applicable, that they are eligible for up to four (4) kinds of relief. It’s important to note that an employer doesn’t have to claim any of these options.

The options on line 22 are:

Qualifying Offer Method

Qualifying Offer Method Transition Relief

Section 4980H Transition Relief

98% Offer Method.

You can’t complete line 22 of Form 1094-C unless you decode the options listed as “certifications of eligibility.” Here’s the scoop on Option A.

Option A, the Qualifying Offer Method, is hard to qualify for. It requires that:

A plan that meets MEC and MV is offered to one or more full-time employees for all months of the year

Employee cost of less than 9.5% of the single federal poverty line; approximately $90 per month for employee only coverage

MEC is offered to spouse and dependents.

What’s the payoff for offering this generous coverage? An employer that meets these requirements can provide a generic “alternative statement” to full-time employees in lieu of the 1095-C. And, the employer can provide a code in lieu of the cost of coverage information on line 15 of Form 1095-C.

What’s the catch? There are several.

The “alternative statement” is not available for a self-insured plan. The employer still has to file the 1095-C with the IRS. The generic form should be reviewed by legal counsel to ensure that it meets the requirements. Employees will compare their form with what their friends from other companies receive and ask a slew of questions.

Once employers know whether they’re an ALE (applicable large employer) and whether they’re part of a controlled group, they have baseline information to help determine just when compliance with the Employer Shared Responsibility (ESR) requirements is required.

Question 3: Have you qualified for transition relief?

Transition relief – or the lack of it – determines when an ALE must be in compliance with the Employer Shared Responsibility provisions of the ACA.

For employers with 50-99 full-time and full-time equivalent employees compliance may be as late as the plan renewal in 2016. Larger employers may have a delayed compliance date corresponding with the start of their 2015 plan year. Notice the use of the word “may” in each sentence. Transition relief is not a foregone conclusion for employers!

There is no short-cut to determining eligibility for transition relief. Employers should walk through the requirements step-by-step. And, it would be prudent for employers to document each step for their files in case questions arise at a later date.

Employers will be required to attest to whether they met the transition relief requirements if they certify they were eligible for it when completing line 22 of Form 1094-C.

Qualification for transition relief – or not – determines when an employer is subject to Section 4980 H penalties. Knowing the answer to this question provides a “date certain” for employer compliance with the “pay or play” provisions of the ACA. This information is critical to assessing benefit offering and employee eligibility options.

A special note of caution to employers with 50-99 full-time and full-time equivalent employees who are contemplating whether to shift their plan’s renewal date to retain their large group status for 2016 – you run the risk of losing transition relief! This would mean that the employer could have to be in compliance as early as January 1, 2015!

Question one (1) of the three (3) questions that employers or their advisers need to have answered yesterday addressed how an employer must count employees for ACA to determine the employer’s size. The next question that employers must be able to answer – Question 2 – is whether the employer is a member of an affiliated group of companies – a controlled group.

Question 2: Are you part of a controlled group?

Whether there is sufficient common ownership among companies to establish controlled group status is key to understanding whether an employer is an ALE (applicable large employer). Controlled group is also referred to by the terms “affiliated” and “aggregation.” Controlled group status is a very complicated facts and circumstances assessment.

What are some of the questions that will help determine whether a controlled group is an issue? These include:

Are there other businesses that the business owner is engaged in?

Might other family members have a business interest?

These and other questions may make an employer an ALE when it may not otherwise seem that they are.

Some business owners may not recognize that they are part of a controlled group. A side hobby-based business totally unrelated to another business, a business owned in part by a spouse or a dependent can all factor in to the determination.

Employers may have assessed controlled group status in the past as it also relates to retirement plans, Medicare Secondary Payer and COBRA, among others.

Tax exempt organizations are also impacted by these rules. In such cases, they are often referred to as “affiliated service groups.”

Entities that are part of a controlled group must count employees of all of the entities to determine if they are an ALE. Controlled group status – and entities comprising the controlled group – must be included in the ACA employer reporting on Form 1094-C.

The IRS chapter that provides the basics to understanding controlled groups is 108 pages long and can be found at www.irs.gov/pub/irs-tege/epchd704.pdf . There is also an excellent webinar (June 2013) on the topic of controlled groups and common law employees archived under NAHU’s Compliance Corner webinars.

Employers who have stayed on the sidelines or merely dipped a toe into ACA compliance now realize that crunch time is rapidly approaching. Large employers will have to report to the IRS about their ACA compliance in early 2016.

For employers or their advisors, there are three (3) questions that need to be answered – yesterday! These questions will determine what an employer’s obligations are and provide a compliance guide map.

This blog covers the first of these important questions.

Question 1: What size employer are you?

What size employer are you?

It’s critical for employers to understand whether they are a large employer or a small employer. In particular, it’s important to determine if an employer is an “applicable large employer” commonly referenced to as the acronym, ALE.

Why is this important? An ALE is subject to the Employer Shared Responsibility requirements – the “pay or play” provisions of the ACA. An ALE is also subject to the Employer Reporting Requirements of the ACA.

The IRS provided a handy formula for a tax forum in 2013. The presentation noted:

This is the simplest formula to determine ALE status. Controlled group rules, seasonal workers and veterans with TRICARE or VA benefits may impact the final sum.

It’s important to understand that an employer’s ACA employer size may – or may not – match the calculation of employer size used by an insurance company to determine available products.

The Surface Transportation and Veterans Health Care Choice Improvement Act of 2015 recently signed by the President doesn’t sound like a law that affects the ACA. Surprise!

This new law amends the section of PPACA that addresses the definition of applicable large employer (Section 4980H(c)(2)).

This provision allows employers to calculate whether they meet the employer shared responsibility requirements as an “applicable large employer” (ALE) by excluding employees enrolled in TRICARE or veteran’s coverage. Of note, employers can recalculate their current status as the effective date of this subsection applies as of January 1, 2014.

A review of IRS documents regarding plans that constitute MEC coverage suggests that not all Tricare or veteran’s coverage may qualify for this counting exception. More guidance will be necessary to understand which programs qualify.

Employers may want to survey whether any employees are covered by these programs. To the extent that an employer’s ALE status may change due to employees covered by these programs, legal advice may be appropriate.

Of note, this new law only affects how an employer counts employees to determine ALE status. These employees are not otherwise excluded from the employer shared responsibility requirements.

Here is the text of the law relating to this change:

SEC. 4007. Amendments to Internal Revenue Code with respect to health coverage of veterans.

(a) Exemption in determination of employer health insurance mandate.—

(1) IN GENERAL.—Section 4980H(c)(2) of the Internal Revenue Code of 1986 is amended by adding at the end the following:

“(F) EXEMPTION FOR HEALTH COVERAGE UNDER TRICARE OR THE VETERANS ADMINISTRATION.—Solely for purposes of determining whether an employer is an applicable large employer under this paragraph for any month, an individual shall not be taken into account as an employee for such month if such individual has medical coverage for such month under—

“(i) chapter 55 of title 10, United States Code, including coverage under the TRICARE program, or

“(ii) under a health care program under chapter 17 or 18 of title 38, United States Code, as determined by the Secretary of Veterans Affairs, in coordination with the Secretary of Health and Human Services and the Secretary.”.

(2) EFFECTIVE DATE.—The amendment made by this subsection shall apply to months beginning after December 31, 2013.

One of the more frequent compliance questions is whether employers need to offer coverage to seasonal employees under ACA. Whether and when a seasonal employee should be offered coverage is particularly important for employers subject to the employer responsibility provisions of the law.

First, it’s important to understand who qualifies as a seasonal employee. In general, a seasonal employee meets the following requirements:

The employee is in a position for which the customary annual employment is six (6) months or less, and

The period of employment should begin each calendar year in approximately the same time of the year.

The final rules reserve the option to more clearly define seasonal employee at a later time.

The rules allow that in unusual instances an employee may still be considered seasonal even if the seasonal employment extends beyond six (6) months. The rules speak to a ski instructor at a resort that has an unusually long or heavy snow season – probably in Boston!

The rules allow that employers may treat seasonal employees that meet these requirements as variable hour employees. As a result, an employer may use the look-back measurement method for seasonal employees in the same manner as variable hour employees.

So, what’s the Bam! in the title mean? The Bam! is that an employee who is hired with the expectation that they will work on average 30 or more hours per week does not have to be treated as a full-time employee for health coverage purposes (and the employer responsibility requirements) if Bam!, that employee is a seasonal employee!

Confusion is a perennial state when addressing application of the rules of ACA – or so it seems. And, one of the more confusing aspects of the law is how to address seasonal employees.

Some of the confusion clears away if you know what question you’re trying to address. If you’re attempting to determine if an employer is an ALE (applicably large employer), then the relevant term is “seasonal worker.”

A seasonal worker means “a worker who performs labor or services on a seasonal basis.” IRS notice 2012-58 defines this term in more detail.

Why is the term “seasonal worker” an important one to understand when assessing whether an employer is an ALE? Seasonal workers are taken into account when counting full-time employees and full-time equivalent employees when determining ALE status.

The final employer responsibility rules provide a “seasonal exception” when determining ALE status. Applying the “seasonal exception” may result in an employer who might appear to be an ALE – and all that ALE status entails – instead exempt and considered to be a small employer.

The “seasonal exception” works as follows:

If the sum of an employer’s full-time employees and FTEs exceeds 50 for 120 days or less during the preceding calendar year, and the employees in excess of 50 who were employed during that period of no more than 120 days are seasonal workers, the employer is not considered to employ more than 50 fulltime employees (including FTEs) and the employer is not an applicable large employer for the current calendar year.

For purposes of the “seasonal exception” four (4) calendar months may be treated as the equivalent of 120 days. Notably, the four (4) calendar months and the 120 days are not required to be consecutive.

This seasonal exception has no affect on whether – or when – a seasonal employee may be determined to be eligible for benefits.