Submitted by Ken Stevenson, Vice President of Employee Benefits at Earl Bacon Agency

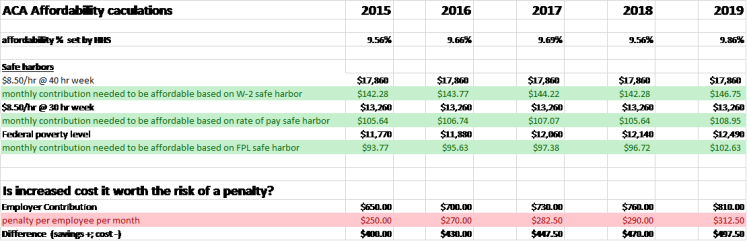

Beginning with Plan years that started in 2015 Applicable Large Employers (50 or more fulltime employees including equivalents in the PRECEDING calendar year) had to concern themselves with a little thing called the “Affordability Threshold”. The original Affordability Threshold was 9.5%. Not a nice neat round 10%. That would have been too easy. Yes 9.5%. Then it became a question of 9.5% of what and the IRS had more answers for that too. But this column isn’t about the rational for the number, the indexing or any of the safe harbors. By now we have learned to live with the Affordability Threshold whether its 9.5% or 9.69%. We’ve, for the most part, figured out which safe harbor or safe harbors to use when filing under 4980H.

This column is about managing the risk of meeting or missing the Affordability Threshold and the consequences it brings.

As agents and brokers, an entirely new demand is being asked of employers and it must be approached with caution. Because the consequences are severe and unlike any experienced before. The IRS doesn’t play, so when an employer calls saying they received a letter from the IRS telling them they are being penalized, guess who is assumed responsible? Remember the letter (IRS letter 226J) is for something that transpired several years ago. Personnel may have changed and/or conversations may have been forgotten since then. But again, this column is not about what to do after getting a letter from the IRS but managing the risk beforehand.

So, let’s look at the risk. You can take the approach of zero risk. In 2019 the Affordability Threshold is 9.86% of annual income and the federal poverty level (FPL) for a single individual is $12,490 in income annually. So that means that an employer using the FPL safe harbor should have their employee’s monthly health insurance contribution be no more than $102.63 for their plan to be deemed affordable ($12,490 / 12 months = $1040.80 monthly income x 9.86% = a maximum contribution of $102.63 ). That puts the employer at ZERO risk of being fined due to failure to meet the affordability threshold. Depending on the industry, economy and labor market, this may be a suitable approach. However, for many employers it’s not economically feasible as using the FPL safe harbor produces the maximum out of pocket for employers. For those employers, it becomes a delicate balance of cost, plan design, multiple plan offerings, choosing a more appropriate safe harbor, measurement and stability options, etc. to avoid the risk of an IRS penalty. Some employers, and brokers, spend large sums of money on affordability calculators or outside consultants to do testing, just to make sure they are not subject to the IRS penalties. They seek ZERO risk. But do they need to? It is worth it? Remember when the ACA passed, and employers were asking is it cheaper to just pay the fine? This may be in a different context but it’s worth exploring.

Here is an example. Employer B&A. B&A typically has around 250 employees. Turnover is high and they elected to use a standard monthly measurement period. There is a wide variance in incomes. About 10% are minimum wage employees which also has the highest turnover. Those employees average only about 3 months employment. It now becomes a simple math problem. The employee contribution is currently $165 per month on their lowest cost plan. Roughly 25 employees will not meet the affordability threshold. Since the group has a 60-day waiting period, the risk exposure is roughly 30 days (90-60) X 25 X $312.50 = $7,812.50. Remember the penalty is prorated monthly. The first option that many employers choose is to increase contribution levels for the whole group and avoid the penalty. B&A determined that if they did that it would cost them an additional $18,000 a year. So while they were at risk of an IRS fine, the cost of that fine was lower than increasing contributions for the entire group. One final point on the application of the penalty. Remember an employer penalty is only applied when a fulltime employee BOTH purchases an individual plan in the Marketplace AND receives a premium tax credit. B&A felt that an even smaller number of those 25 “at risk” employees would meet that criteria. Most were young and either on their parents plan or buying health insurance was just not a priority for them. So that $7,812.50 penalty risk would most likely be much less and they were willing to accept that.

In this case accepting some risk was worth it for the employer. But its important to document a conversation like this because there is still nothing more frightening for an employer than seeing that IRS letterhead.