Many employers are struggling with the ACA’s employer reporting requirements. It’s hard enough to know what to report when an employee enrolls in coverage. But, what is the proper way to report that an employee has waived coverage?

Line 16 becomes very important in this scenario. If the employer has adopted an affordability safe harbor, the code for the chosen safe harbor will appear in line 16.

There are three (3) safe harbor affordability codes. These are:

- 2F The W-2 safe harbor (Box 1 of the W-2)

- 2G The Federal Poverty Line safe harbor

- 2H The rate of pay safe harbor.

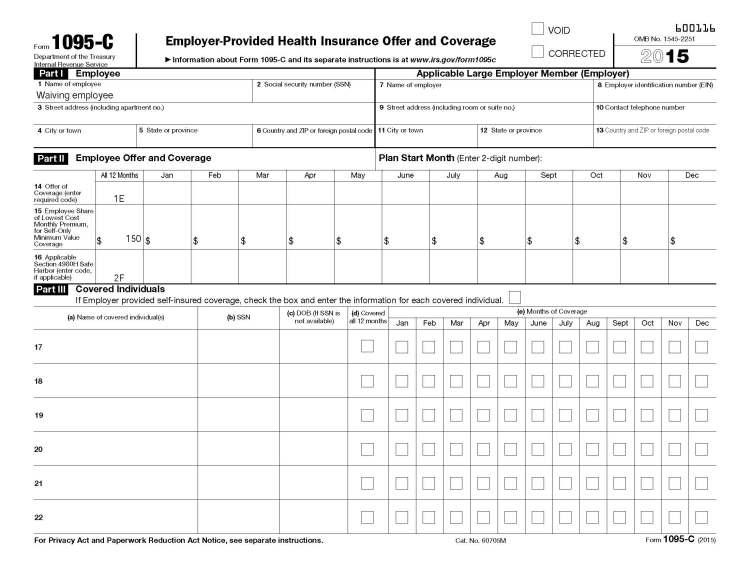

The example below shows code 2F. However, depending on the employer and the employee class, the safe harbor method used may vary. Of particular importance, the W-2 safe harbor must be used for all months of the calendar year for which the employee was offered health coverage.

For an IRS FAQ that describes the safe harbors see question 19 here.

If an employer has not opted to use a safe harbor, line 16 would be left blank (assuming no other codes are applicable such as transition relief). By doing so, the employer is indicating to the IRS that the employer and/or the employee may be subject to a penalty.

If an employer offers a self-funded plan, Part III of form 1095-C would also be left blank when an employee has waived coverage.

Given the penalties that employers may face if an employee does not have coverage or is not offered coverage , the importance of documenting that an employee has been offered coverage and declined it becomes even more important. Employers should obtain a signed waiver from any employees that waive coverage. In the event that an employee does not return a signed waiver, employers should note in enrollment materials that failure to respond by a certain date will be assumed to be a waiver of coverage.

Example when Employee Waived an Offer of Coverage

Facts of Assumptions:

- Employer offers insured plan

- Coverage for lowest cost employee premium per month is $150

- The employee, spouse and dependents were offered coverage for all 12 months

- The employer has offered affordable coverage using the W-2 safe harbor

- The employee has waived coverage for everyone in the family.